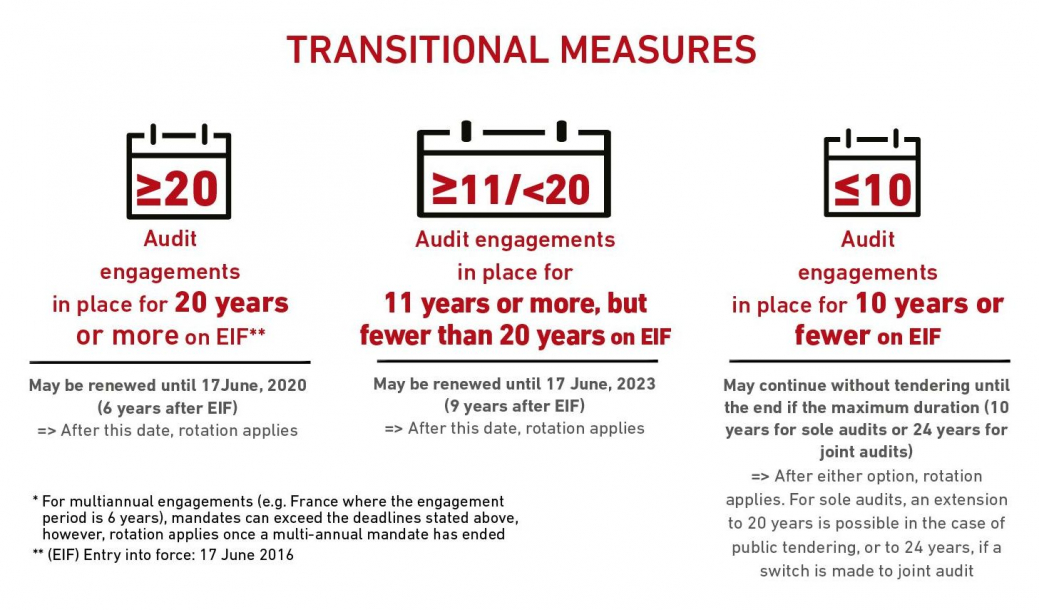

Its purpose is to avoid disruptive change and to provide the market with a smooth transition to cope with the new measures. Transitional measures vary depending on the length of the audit appointment at the date of Entry into Force (EIF): 17 June 2014.

- If the auditor has been in place for 20 years or more at EIF, the last renewal must take place before 17 June 2020.

- If the auditor has been in place for fewer than 20 but more than 11 years, the last renewal must take place before 17 June 2023.

- For all other engagements, the new regime will apply.

The following factors should be considered when determining the seniority of mandates:

- The transitional period that applies will be determined based on the tenure of the engagement at the date of EIF.

- The duration of the audit engagement will be counted from the first financial year covered in the audit engagement letter in which either the statutory auditor or the audit firm was first appointed to carry out the consecutive statutory audits for the PIE.

- This calculation must consider other firms that the audit firm of the PIE has either acquired or merged with, starting from the date the audited entity became a PIE.

Testimonies